Beyond Growth: What H1 2026 Really Told Us About the Future of Digital Banking

- Javier Guevara

- Jul 2

- 8 min read

The industry's biggest announcements weren't telling different stories. They were all pointing towards the same strategic shift.

If you had followed digital banking only through headlines during the first half of 2026, you would probably conclude that the industry was moving in several different directions at once.

AI dominated the conversation.

Digital banks expanded into wealth management.

SME platforms strengthened treasury capabilities.

Infrastructure providers accelerated Banking-as-a-Service.

Global banks renewed their digital ambitions across Europe.

At first glance, these appear to be unrelated developments.

They aren't.

After analysing hundreds of announcements during H1, we believe they all point towards the same strategic question:

How do financial institutions continue expanding without making their businesses more complex, fragmented and difficult to manage?

That question is quietly redefining competition.

For much of the past decade, success in digital banking was easy to measure.

More customers.

More products.

More markets.

More growth.

Expansion itself became the strategy.

Today, digital banking no longer needs to prove it works.

It needs to prove it can endure.

Leadership teams are increasingly asking a different question:

How do we turn growth into a stronger business rather than simply a bigger one?

That helps explain why many of H1's biggest announcements initially appeared unrelated.

Revolut continued expanding across Business Banking, lending and wealth management.

Monzo showed that becoming a customer's primary bank is increasingly more valuable than simply adding another account.

N26 reached its first full year of profitability.

Allica Bank demonstrated that focused execution can outperform broad expansion.

Trade Republic continued strengthening long-term customer relationships by combining saving, investing and everyday banking into a single proposition.

Different institutions.

Different strategies.

The same objective.

Digital banking is no longer a race to launch more products.

It is becoming a race to make more products work together.

Growth remains essential.

But growth alone is becoming a weaker competitive advantage.

The market is increasingly rewarding institutions that deepen customer relationships rather than simply broaden customer bases.

Yet this changing definition of growth only explains part of what happened during H1.

An even bigger shift is beginning to emerge.

As financial institutions expand, products are no longer simply adding functionality.

They are reshaping how financial institutions operate.

And that may prove to be the defining strategic shift of 2026.

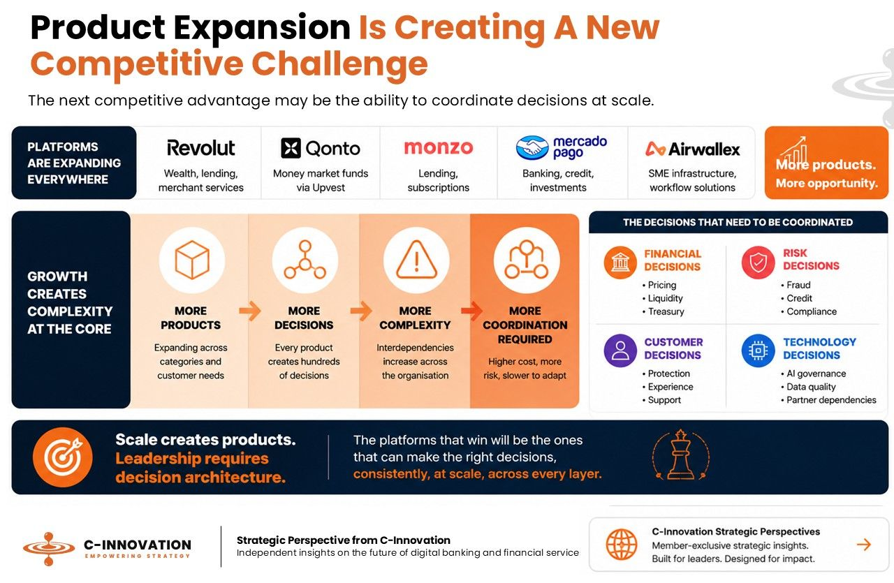

The first half of 2026 demonstrated that product expansion is no longer simply creating new revenue opportunities. Every additional capability also creates new financial, operational, regulatory and technology decisions. As institutions continue expanding across wealth, lending, treasury, infrastructure and AI, competitive advantage increasingly depends on their ability to coordinate those decisions through a coherent operating model.

The biggest product announcements weren't really about products

At first glance, H1 looked like another period of rapid product innovation.

Digital banks expanded into wealth management.

SME platforms strengthened treasury capabilities.

Infrastructure providers accelerated Banking-as-a-Service.

The obvious conclusion was that competition was becoming broader.

In reality, something much more significant was happening.

Financial institutions were no longer launching products simply to expand their portfolios.

Increasingly, every new capability was changing how the business itself operates.

A wealth proposition strengthens customer relationships.

A treasury platform moves a bank closer to the centre of a company's financial operations.

A banking licence reshapes funding, economics and strategic independence.

Products are no longer standalone features.

They are becoming building blocks of much larger financial systems.

Several announcements during H1 illustrate this shift.

When bunq launched bunq-as-a-Service, it transformed its banking licence into infrastructure that other organisations can build upon. Rather than serving only its own customers, bunq expanded the role its platform can play across the wider financial ecosystem.

Wise followed a similar path. Through Wise Platform, it increasingly enables banks and financial institutions to embed international payments into their own customer journeys, monetising the infrastructure behind those interactions.

The same pattern emerged elsewhere. Starling continued expanding Engine, Lunar launched Moonrise, and Qonto strengthened its SME proposition through treasury and investment capabilities, each moving beyond traditional banking products towards broader financial platforms.

Different products.

The same strategic objective.

How do we build a business that becomes more valuable every time another capability is added?

That marks an important shift from the previous generation of digital banking, where success was often measured by the number of products a bank could launch.

Today, competitive advantage increasingly depends on how well those products work together.

Payments strengthen treasury.

Treasury supports lending.

Lending deepens customer relationships.

Wealth increases engagement.

Infrastructure creates new revenue opportunities.

Every capability reinforces the next.

The winners won't build the biggest product portfolios.

They'll build the most connected ones.

Looking back, this may prove to be one of the defining strategic shifts of H1 2026.

The market is moving away from competing through individual products and towards competing through the quality of the operating model connecting those products together.

That transition also explains why AI has become far more than another technology trend.

As products become increasingly connected, financial institutions are no longer trying to automate individual tasks.

They are beginning to automate decisions.

And that changes the competitive conversation entirely.

The next competitive advantage is decision quality

As financial institutions build more connected operating models, another shift is becoming increasingly visible.

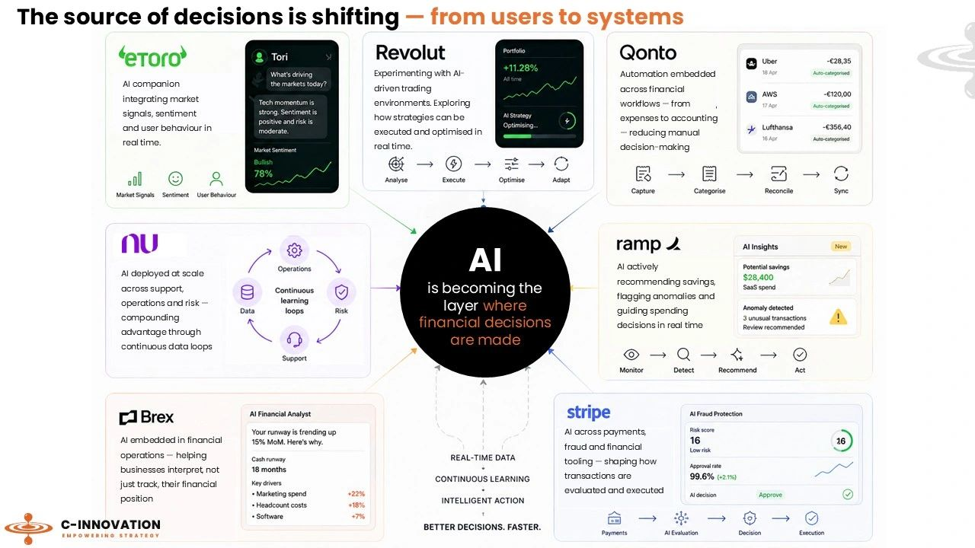

AI is moving from assistance to execution.

Much of the industry's conversation has focused on AI-powered assistants, chatbots and productivity tools. Those developments matter, but they are unlikely to define the next phase of competition.

The bigger opportunity lies elsewhere.

AI is beginning to influence how financial institutions make decisions.

The Next Competitive Advantage Is Decision Quality

Across H1 2026, AI adoption accelerated across very different business models. Yet the strategic direction was remarkably consistent. Whether supporting investment decisions (eToro), financial operations (Brex), payments (Stripe), banking (Revolut), expense management (Qonto), spending optimisation (Ramp) or customer operations (Nubank), AI is increasingly moving beyond productivity to become part of the financial decision-making process. The competitive advantage is no longer simply deploying AI—it is deciding where AI should make decisions and how those decisions are governed.

That changes the strategic conversation.

The question is no longer "How do we use AI?"

It is "Where should AI make decisions—and where should humans remain in control?"

The institutions that create the greatest advantage will not necessarily be those deploying the most AI features.

They will be those using AI to simplify operations, improve decision quality and strengthen customer outcomes without increasing organisational complexity.

As AI becomes embedded across the financial operating model, competitive advantage will depend less on the technology itself and more on how effectively institutions govern, integrate and trust it.

That is likely to become one of the defining strategic questions of the second half of 2026.

Competition is no longer starting inside the bank

Perhaps the most important lesson from H1 is that banks are no longer competing only with other banks.

Increasingly, they are competing with whoever controls the moment a financial decision is made.

That shift is easy to overlook because it doesn't always look like banking.

When Apple expands the financial capabilities within its ecosystem, it isn't trying to build a traditional bank. It is making financial services part of a broader customer experience. Payments, savings and financing become almost invisible, integrated into journeys customers already trust.

We see a similar direction in Europe. Goldman Sachs' preparations to launch Marcus in Ireland and JPMorgan's continued digital expansion demonstrate that global institutions increasingly see Europe as a strategic digital banking market. Their ambition is not simply to win customers; it is to become part of more financial relationships.

The same principle applies to infrastructure providers. Starling's Engine, Lunar's Moonrise, Wise Platform and bunq-as-a-Service are not competing for the same customers in the traditional sense. They are enabling other organisations to embed financial services into their own customer experiences, extending their influence far beyond their own brands.

Viewed individually, these are very different strategies.

Viewed together, they point towards the same conclusion.

Financial services are becoming increasingly embedded within broader digital ecosystems.

Customers are no longer thinking, "I need to use my bank."

They are thinking, "I need to complete a task."

Pay a supplier.

Book a trip.

Manage company cash flow.

Split a bill.

Receive financial advice.

Move money internationally.

Increasingly, those moments begin outside the traditional banking app.

That changes the competitive challenge for every financial institution.

Success is no longer determined only by the quality of individual products. It increasingly depends on whether an institution can position itself at the centre of the customer's financial life, regardless of where that interaction begins.

Looking back, the biggest announcements of H1 may have appeared unrelated.

Looking forward, they increasingly look like different expressions of the same strategic transition.

The industry is no longer competing to build the largest collection of financial products.

It is competing to build the most coherent financial platform—one capable of connecting products, intelligence and customer relationships into a single operating model.

And that is likely to become the defining competitive advantage of the second half of 2026.

What H2 2026 Is Likely to Separate

The first half of 2026 was not defined by a single product launch, technology breakthrough or competitive move.

It was defined by a gradual shift in how competitive advantage is being created.

Looking back, many of the year's biggest announcements appeared unrelated.

Revolut expanded its ecosystem.

Monzo deepened primary banking relationships.

N26 reached profitability.

bunq turned its banking licence into infrastructure.

Wise continued strengthening its platform strategy.

Starling and Lunar opened their technology to partners.

Apple embedded financial services more deeply into its ecosystem.

AI became part of almost every strategic conversation.

Viewed individually, these were different stories.

Viewed together, they point towards the same conclusion.

The industry is entering a new phase where competitive advantage will depend less on how much institutions add, and more on how effectively they connect what they already have.

That is likely to shape the second half of 2026.

We expect the market to place greater emphasis on four areas.

First, the quality of customer relationships rather than customer acquisition alone. Institutions that increase engagement, deposits and recurring revenues will increasingly outperform those focused primarily on adding users.

Second, the coherence of the operating model. As product portfolios continue expanding, leadership teams will need to ensure every new capability strengthens the overall business rather than adding unnecessary complexity.

Third, the ability to deploy AI where it genuinely improves decision quality. The competitive advantage will not come from introducing more AI features, but from using AI to simplify execution, strengthen governance and improve customer outcomes.

Finally, the ability to remain present at the moments that matter most. As financial services become increasingly embedded within broader digital ecosystems, institutions will compete not only through their own channels, but through the environments where customers already live, work and make financial decisions.

None of these developments suggest that growth is becoming less important.

Quite the opposite.

Growth remains essential.

But the definition of growth is changing.

The institutions most likely to lead the next phase of digital banking will not necessarily be those launching the most products, entering the most markets or announcing the most AI initiatives.

They will be those that can combine growth, product, AI and customer relationships into a coherent operating model that becomes stronger—not more complex—as it expands.

That is perhaps the most important lesson from the first half of 2026.

The biggest strategic shift wasn't AI.

It wasn't wealth management.

It wasn't Banking-as-a-Service.

It wasn't international expansion.

Those were all visible expressions of something much more fundamental.

The industry is moving beyond building digital banks.

It is beginning to build integrated financial platforms.

And in the years ahead, the winners are unlikely to be those with the broadest product portfolios.

They will be those with the clearest strategy for connecting every product, every capability and every customer relationship into a single, coherent financial system.

Enjoyed this perspective? Discover more through C-Innovation membership, including weekly strategic insights, market research and benchmarking.

Comments